Inside Xiaomi’s sharp downfall in India: Poor product positioning, retailer dissatisfaction and more

For nearly half a decade, Xiaomi was synonymous with smartphone dominance in India. From 2017 to 2022, the Chinese brand, often regarded as the “Apple of China”, sat atop the market, riding on the twin engines of high-spec devices at unbeatable prices and a fiercely loyal online customer base. But in a stunning reversal of fortune, the Chinese phone maker seems to have lost its grip on the market. Not only that, there are more serious issues affecting its presence in the Indian market. These include poor positioning of products, objectionable pricing of devices and dissatisfaction among retailers.

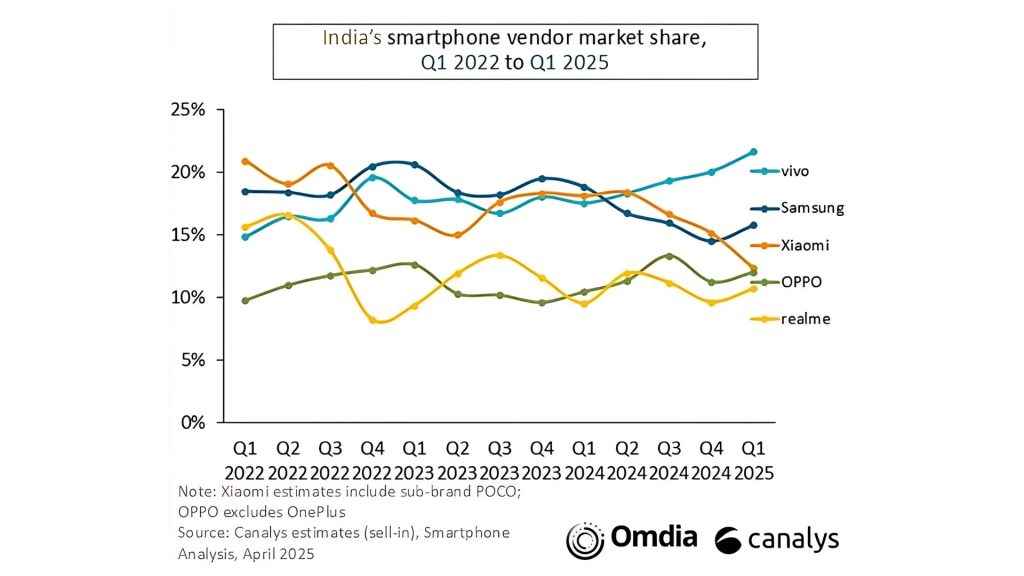

According to IDC, Xiaomi plummeted to seventh place in the Indian smartphone rankings, a fall as spectacular as its earlier rise. The latest Canalys data paints an equally grim picture as Xiaomi’s shipments dropped by 38 per cent year-on-year in Q1 2025, despite major launches like the Redmi Note 14 series and Xiaomi 15 in the same period. This is the sharpest decline in shipments among all major brands operating in India.

Source: Canalys Smartphone Market Pulse (Q1 2025)

The company that revolutionised India’s smartphone landscape with its “more bang for your buck” philosophy now finds itself fighting for relevance in the same country. So what went wrong for a brand that once seemed invincible? Digit’s conversations with leading industry analysts, market experts, and retail insiders reveal a complex mix of strategic missteps, execution gaps, and intensifying competitive pressure, factors that together turned Xiaomi’s triumph into turmoil.

Xiaomi: The Fall of a Giant

Xiaomi’s dominance, which stretched from 2017 to 2022, has eroded dramatically. Even with the launch of its Redmi Note 14 series and Xiaomi 15 flagship, the brand’s market share has shrunk to just 12 per cent, dropping it from market leader to third place before sliding further to seventh by January.

Navkendar Singh, Associate Vice President of IDC India, points to a combination of factors. “It has faced inventory issues in 2024 and new models launched in 2025 have received lukewarm response,” he explains. Meanwhile, competitors like Vivo have maintained “a growth trajectory for the past several quarters with strong play in volume-driven mass segment and offline channel.”

Shubham Singh, Research Analyst at Counterpoint Technology Market Research, confirms the decline.

“Xiaomi witnessed a sharp 37 per cent YoY decline in Q1’25, primarily due to higher inventory, which led Xiaomi to adopt a cautious stance with a focus on stock clearance. Despite recent launches like the Redmi Note 14 series, Redmi 14C 5G, and A4 5G, consumer traction has remained limited. The brand continues to face headwinds, especially as competition intensifies across segments,” he said.

A Shift in Strategy, A Loss of Identity

A major internal factor behind Xiaomi’s decline has been its confused brand positioning. Traditionally, the Redmi brand was loved for offering unbeatable value-for-money devices. However, as Faisal Kawoosa, Chief Analyst at TechARC, points out, Xiaomi’s attempt to premiumise Redmi has backfired.

[Xiaomi] lost the perception battle.

Faisal Kawoosa, Chief Analyst at TechARC

“Redmi is known for its ‘value for money’ positioning. The moment it tried to go premium, without much preparation, it lost the perception battle,” said Kawoosa. “Premium pricing requires brand trust and aspirational pull, something Redmi wasn’t ready for yet.”

Tech analyst and market insights expert Yogesh Brar agrees that this premiumisation push has created a “fragmented” brand identity stuck between “its budget roots (Redmi/Poco) and premium aspirations (Xiaomi series), which may confuse consumers and dilute its image.”

Prabhu Ram, VP of Industry Research Group at CyberMedia Research (CMR) notes that while “Xiaomi is currently undergoing a brand realignment and reinvention, with its recent premium strategy beginning to deliver positive results,” the company needs to “significantly strengthen its marketing and communications to enhance brand salience, particularly among Gen Z consumers.”

Xiaomi is currently undergoing a brand realignment and reinvention.

Prabhu Ram, VP of Industry Research Group at CyberMedia Research (CMR)

Rising Competition and the Offline Blind Spot

Most critically, Xiaomi has struggled to translate its online success to physical retail stores, while rivals like Vivo, Oppo, and even Motorola seized the opportunity to strengthen their hold, particularly in the offline market, which today accounts for nearly half of smartphone sales in India.

Brar underscores this point, calling 2025 a “channel-driven year” where “offline execution is key to gaining share, especially with the fragile demand.” He notes that “Xiaomi’s historical online strength is less advantageous now” as it faces “reported weaknesses or friction in offline channels compared to competitors like Vivo.”

Offline execution is key to gaining share, especially with the fragile demand.

Yogesh Brar, Tech analyst and market insights expert

According to Navkendar Singh of IDC, “Vivo has been on a growth trajectory for several quarters, with a strong presence in the volume-driven mass segment and a powerful offline channel.”

The most stunning insights came from Kailash Lakhyani, Founder Chairman of AIMRA (All India Mobile Retailers Association), who revealed that retailers aren’t particularly happy with the way Xiaomi is operating in India.

“There is poor engagement with retailers by the Xiaomi team. Xiaomi promoters are demotivated, salaries are low, incentives are weak. Retailers earn better margins with Vivo and Oppo, so naturally, they push those brands more,” he revealed, while mincing no words.

There is poor engagement with retailers by the Xiaomi team.

Kailash Lakhyani, Founder Chairman of AIMRA (All India Mobile Retailers Association)

Retailers who were once enthusiastic about Xiaomi now find it bureaucratic, slow to respond, and out of touch with grassroots realities. According to Lakhyani, Xiaomi’s high pricing, lack of “pull models,” and complicated dealer incentives have alienated its critical distribution base.

“Any brand today has to equally focus on online and offline channels as these have attained an equilibrium and are contributing almost equal business in terms of volumes,” explains Kawoosa. “For the past few years it has been a gap for Xiaomi.”

Retailer Relations in Shambles

Lakhyani paints a damning picture of Xiaomi’s relationship with its retail partners:

“There is a poor relationship with AIMRA – All India Mobile Retailers Association from 2024 onwards so they [Xiaomi] are not getting the ground realities and the right inputs which AIMRA gives to Vivo, Oppo and Realme,” he states bluntly.

“Consumers are not showing interest in Xiaomi products priced above Rs 15,000, but they are buying Vivo and Oppo devices like Y-Series and V-series and T-series, whereas Oppo A-series, K-series and F-series are selling great,” Lakhyani reveals.

Consumers are not showing interest in Xiaomi products priced above Rs 15,000.

Kailash Lakhyani, Founder Chairman of AIMRA (All India Mobile Retailers Association)

Lakhyani went on to detail a series of missteps in Xiaomi’s retail strategy. “Retailers purchase approximately 300 units in total sales, with Xiaomi accounting for 9% Margin and Vivo/Oppo for 13% Margin, so a gap of 4% is why retailers are showing more interest in Oppo & Vivo,” Lakhyani explains.

This significant margin differential creates a clear financial incentive for retailers to prioritise competing brands.

The gap persists even among smaller retailers: “Small retailers sales of Xiaomi and Vivo/Oppo sell around 100 units each, representing 7% margin in Xiaomi and 9% Margin OPPO/VIVO.” When operating on thin margins, even these seemingly small percentage differences significantly impact retailer profitability and motivation.

Xiaomi has a unique sell-in and sell-out strategy that no other company employs.

Kailash Lakhyani, Founder Chairman of AIMRA (All India Mobile Retailers Association)

In addition, Lakhyani highlights a uniquely rigid approach that alienates retail partners: “Xiaomi has a unique sell-in and sell-out strategy that no other company employs. For example, if an outlet has a sell-out target of Rs 10 lakh, they must achieve a sell-in of Rs 8 lakh to be eligible for the scheme payout; otherwise, no payout is given to the dealer.”

This all-or-nothing approach leaves retailers vulnerable and frustrated, with Lakhyani noting the consequences in stark terms: “So many retailers are not interested in Xiaomi’s business.”

Even more damaging is Xiaomi’s approach to setting and managing retailer targets, Lakhyani says. “For example, if a retailer’s average sales volume over the past three months is 50 units, with an average value of Rs 6 lakh, Xiaomi should ideally set an initial target of Rs 6.5 lakh and gradually increase it. However, they directly set a target of Rs 7.5 lakh, and when retailers request a revision, they are told that no revisions will be entertained.”

He explicitly criticises the company’s communication style: “When retailers request target revisions, they are often denied and spoken to arrogantly. This is damaging retailers’ sentiment and trust.”

Most recently, Xiaomi has implemented a fundamental change to its incentive structure without adequate preparation: “Recently Xiaomi has changed its sell-out scheme payout strategy from volume-based to value-based.”

Lakhyani argues this approach is fundamentally misaligned with Xiaomi’s historical positioning. “This approach is likely to fail because Xiaomi has historically focused on volume. If they want to shift to a value-based strategy, they need to give retailers time to adapt,” he adds.

“From day one, Xiaomi was a pull brand due to Online modus operandi but after ED raids many top brains left Xiaomi. However, due to poor model placement and pricing strategies, it has now become a push brand,” says Lakhyani.

Xiaomi has been aiming for a balanced omnichannel play.

Navkendar Singh, Associate Vice President of IDC India

This sentiment is echoed by Singh of IDC, who notes, “Xiaomi has been aiming for a balanced omnichannel play, however competitive pressure and soft demand for some of its key models in offline has impacted its performance for past several quarters.”

A Perfect Storm in Tier 2 and Tier 3 Markets

Perhaps most painful for Xiaomi is the erosion of its dominance in Tier 2 and Tier 3 cities, once the backbone of its India success story, to players such as Motorola, Lava and Infinix.

“Yes, smaller brands like Motorola, Infinix, and Lava are finding success here. These are not challengers to Xiaomi alone, but to all players including Samsung,” says Singh.

Aggressive challengers such as Nothing and Motorola are gaining traction in the value-for-money segment.

Prabhu Ram, VP of Industry Research Group at CyberMedia Research (CMR)

Prabhu Ram notes that “aggressive challengers such as Nothing and Motorola are gaining traction in the value-for-money segment,” precisely the space where Xiaomi once dominated.

Kawoosa agrees that Xiaomi has miscalculated in its traditional strongholds: “I wouldn’t say Xiaomi, but yes Redmi is being overlapped by these brands. Perhaps, Xiaomi felt that its Redmi can command a premium in this segment considering the challenger brands also forayed in. But, this segment is extremely price sensitive, and Redmi portfolio automatically started appearing out of bounds for the segment buyers.”

Xiaomi should drop the prices [of Note 14 series] upto Rs 3000.

Kailash Lakhyani, Founder Chairman of AIMRA (All India Mobile Retailers Association)

Lakhyani specifically points to the Note 14 Series: “The phone is good, but its price is high, resulting in no customer demand. Xiaomi should drop the prices upto Rs 3000.”

The Vivo Contrast

Vivo gained 13 per cent YoY in the same period Xiaomi stumbled by 38 per cent. So, what explains this trajectory?

Vivo has invested in building offline capability since it forayed in India, a decade ago.

Faisal Kawoosa, Chief Analyst at TechARC

“Rome is not built in one day,” explains Kawoosa. “Vivo has invested in building offline capability since it forayed in India, a decade ago. Xiaomi for initial 6 years or so was predominantly online. So it takes time.”

Brar provides a more detailed breakdown of Vivo’s success formula. Vivo excelled through a balanced online-offline strategy with a strong retail presence,” he explains, pointing to a decade of methodical channel relationship building that Xiaomi has struggled to match.

Brar highlights Vivo’s strategic product segmentation, noting how the company effectively leverages “different series (V, T, Y) for various segments and channels,” creating clear value propositions for different consumer groups.

Finally, Vivo’s marketing efforts have resonated strongly with Indian consumers. Brar points to “effective marketing campaigns” including the premium ZEISS partnership, targeted wedding season promotions, and strategic use of influencers that have significantly boosted the brand’s visibility and appeal.

Xiaomi & the Path to Recovery

The Indian smartphone market in 2025 is expected to be flat in volume but growing in value, driven by premiumisation trends. Replacement cycles are elongating (up to 22 months), and economic headwinds have made buyers cautious. In such an environment, Xiaomi faces a tough but not insurmountable road to recovery.

Xiaomi will have to chart out different paths for Redmi and Xiaomi as brands.

Faisal Kawoosa, Chief Analyst at TechARC

Kawoosa advises Xiaomi to maintain separate identities for its brands. “Xiaomi will have to chart out different paths for Redmi and Xiaomi as brands. These paths must reflect the positioning and do justice with the product and the experience it promises to the customers in these segments.”

Ram sees hope in Xiaomi’s premium strategy but emphasises the need to “significantly strengthen its marketing and communications to enhance brand salience, particularly among Gen Z consumers.”

According to Brar, Xiaomi must urgently: rebuild retailer relationships while clearing excess inventory; create distinctive mid-premium products with clear competitive advantages; respond nimbly to market shifts with flexible financing options; and craft compelling messaging that clearly communicates why consumers should choose Xiaomi over increasingly aggressive rivals.

“The brand needs to stay unambiguous, deliver strong partner relations, and effectively communicate differentiated value to consumers. Tactical but noticeable changes can help it rebound,” Kawoosa aptly summarizes.

Xiaomi’s fall from the top is a cautionary tale for tech brands everywhere: success is never permanent, and misreading the market, neglecting core partners, or overestimating brand power can swiftly reverse fortunes.

India’s smartphone story is still being written. Xiaomi has the infrastructure, talent, and product prowess to mount a comeback. But it must act decisively before it risks becoming a footnote in a market it once ruled.

We reached out to Xiaomi for a comment, but did not receive a response by the time of publication.

(Note: The analyst’s comments and quotes have been edited for veracity.)

Also Read: How Motorola Is Quietly Taking Over India’s Smartphone Market