“There have been a lot of new developments over the course of the last 12 months in this market.” That is how Salone Sehgal, Founder and Managing Partner of Lumikai, India’s pioneering interactive media and games VC fund, opens her conversation with Digit around the firm’s State of India Interactive Media Report 2025. The report puts the country’s interactive media economy at $13.8 billion, growing at 17% year on year, spanning video, gaming, social media, animation and audio. And cutting across all of it, quietly but decisively, is AI.

Also read: Zuckerberg wants AI CEO to run Meta: What could go wrong?

One of the first things Sehgal addresses is the India versus Bharat question that has dominated conversations in both government and tech circles. Her answer is unambiguous. “There is almost no difference between what a tier one user or an India user is consuming vis-a-vis a Bharat user,” she says. The report backs this up with 877 million smartphone users, data costs at $0.10 to $0.15 per gigabyte, 5G rolled out across 99.8% of districts, and UPI now handling 85% of all payment transaction volume in the country. Rural smartphone ownership now exceeds urban at 63% versus 37%. For anyone building in this space, the next hundred million users are not coming from metros.

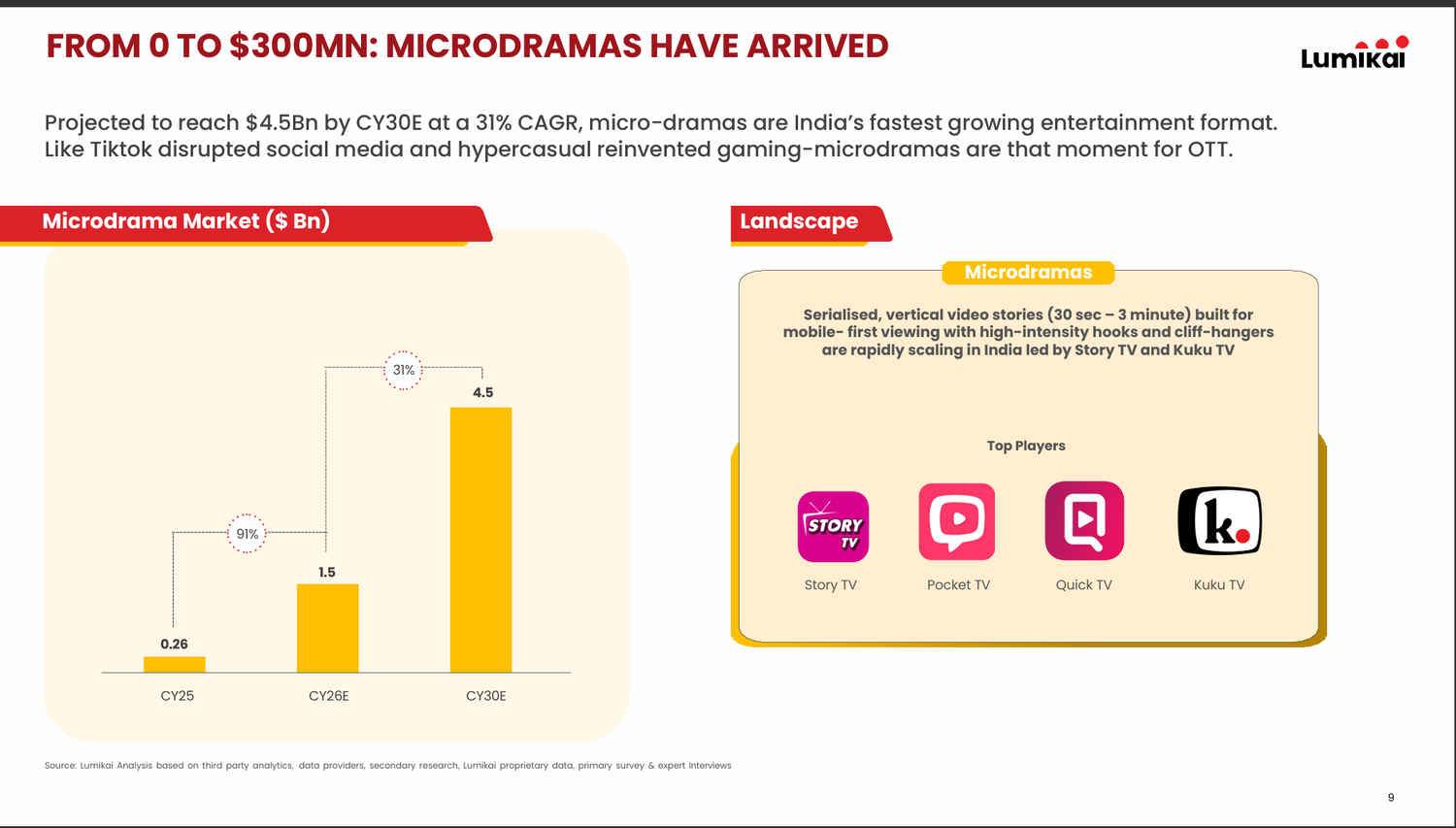

If there is one finding that captures the imagination, it is the rise of microdramas. Sehgal describes it as one of her biggest surprises. “The emergence of microdramas as a category, which is largely a 10-month-old industry, and the speed at which it has grown,” she says, was something the team did not fully anticipate. The report shows this market went from virtually zero to $260 million in CY25, with OTT having taken nearly three years to reach comparable numbers. Platforms like Story TV and Kuku TV are dropping four episodes a day, a production velocity made possible largely by AI. The report projects this market will hit $4.5 billion by 2030. Sehgal believes microdramas and OTT can coexist. “It’s snackable content, it fills a spot in a viewer’s daily life, like when a person is commuting,” she says. That may be true, but at the pace microdramas are closing the gap, OTT platforms would be unwise to treat this as anything less than a structural shift.

Also read: Fuelling in India: Nawgati’s mapping app wants to make it more convenient

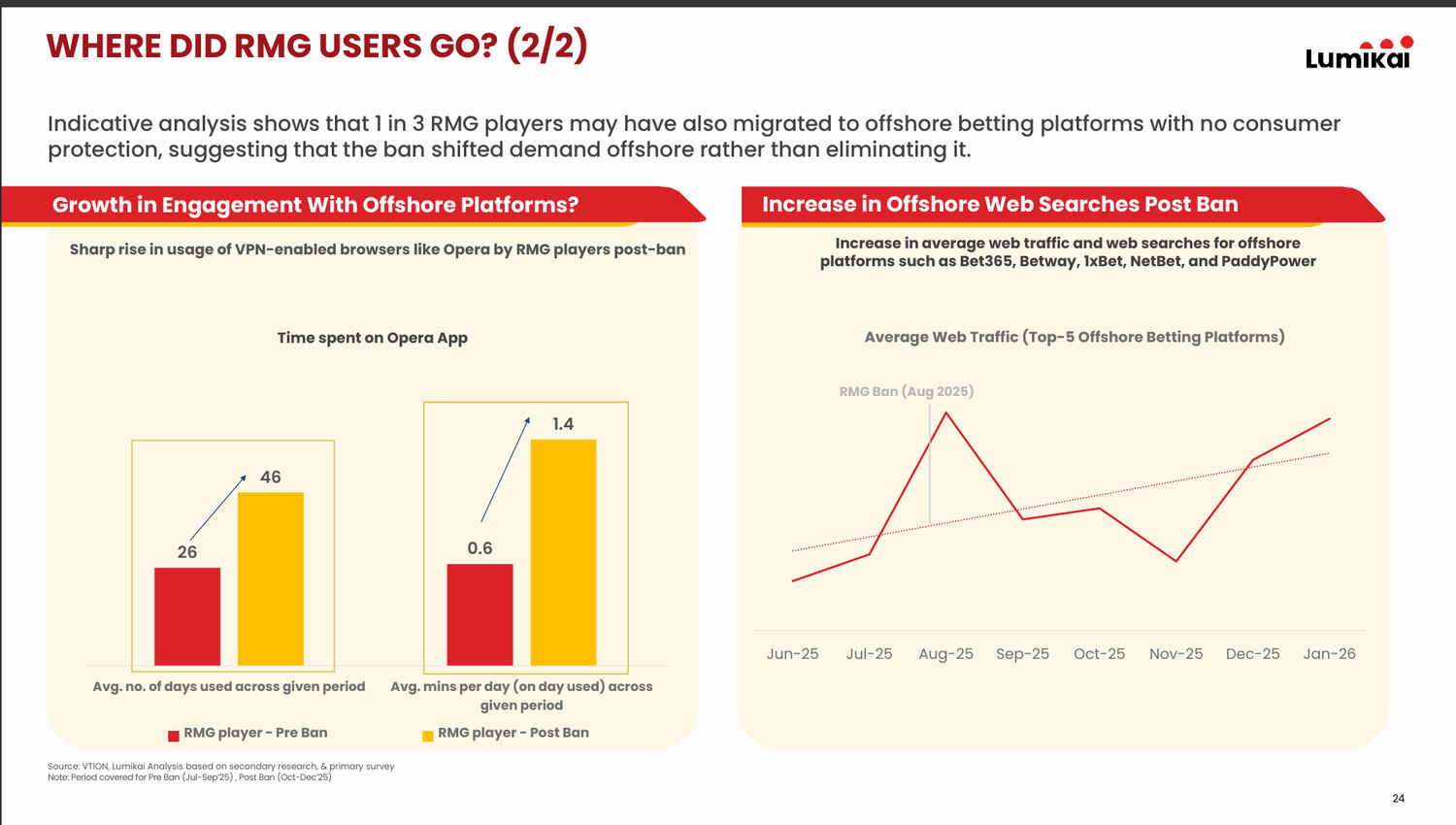

India’s ban on Real Money Gaming in August 2025 was one of the most consequential regulatory decisions in the country’s digital history. Sehgal is careful not to opine on its efficacy, but the data tells its own story. “The ban has, to some extent, redirected demand rather than eliminated it,” she says. The report, using data from 100,000 smartphone users tracked by consumer insights platform VTION, found that 1 in 3 RMG players appear to have migrated to offshore betting platforms like Bet365 and 1xBet, with zero regulatory oversight and no consumer protection. Banning a behaviour without building an alternative does not make it disappear. It just moves it somewhere harder to regulate.

If microdramas were the loudest surprise in this year’s report, audio was the quietest. “We didn’t actually expect audio to come out. It’s a sleeper category. We didn’t anticipate that,” Sehgal says. The report shows audio growing at 29% to hit $400 million in CY25, making it the fastest growing category in the entire report. What is driving it is not music streaming alone but the rise of episodic audio storytelling on platforms like Kuku FM and Pocket FM. The report shows audio series generating 1.7 times more daily time spent than music streaming at 31 minutes per day versus 18. It turns out Indians are willing to pay for a good story regardless of whether it comes with visuals. For a market that has historically been dismissed as too distracted for long-form audio, that is a meaningful shift in behaviour.

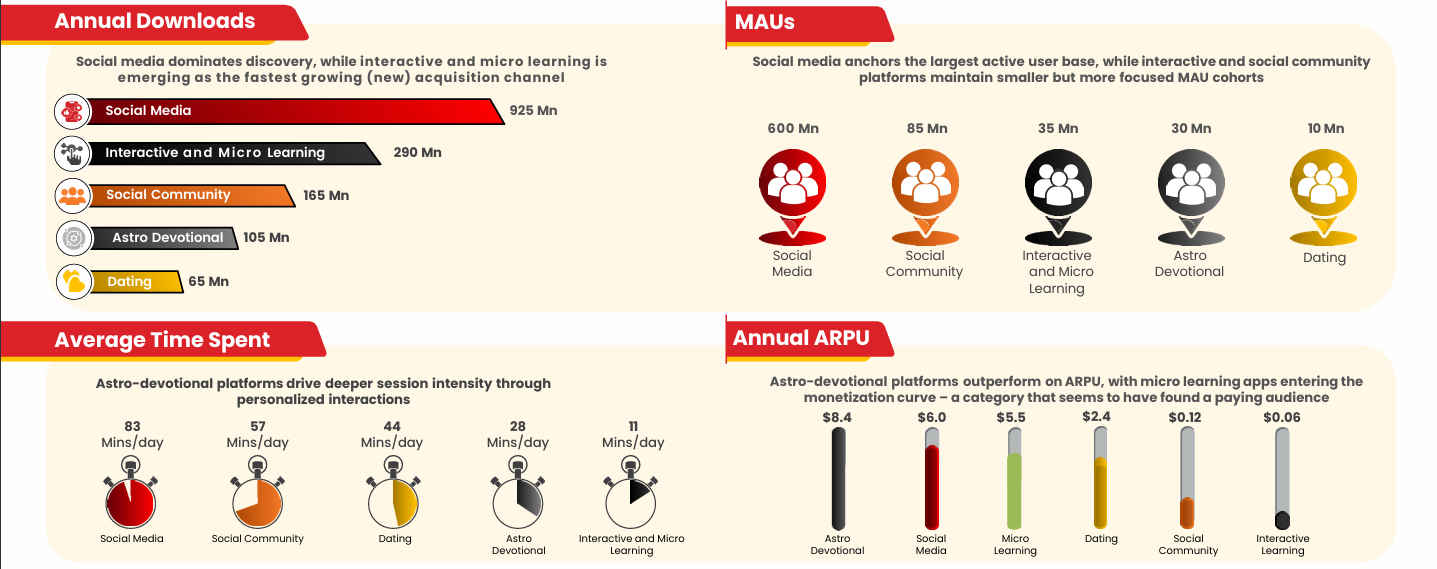

One of the report’s revelations is that astro-devotion platforms command the highest ARPU in the entire social and community category at $8.4 annually, outpacing even dating apps and social media. Sehgal’s explanation is straightforward. “India has always been a faith-based economy. Post-COVID that behaviour has just moved online,” she says. Platforms like AstroTalk and Lumikai portfolio company Ask My Guru are seeing users come with pressing questions about marriage, career and family. The anonymity and personalisation these platforms offer is what drives willingness to pay. As Sehgal puts it, these platforms solve for high intent rather than capitalising on habit and boredom.

Across every segment of the report, AI’s fingerprints are visible. The report shows animation studios cutting production timelines by 50% with productivity uplifts of 25%. Gaming studios are using AI for asset creation and predictive economics. But when asked whether AI is replacing human workers the way it is in global big tech, Sehgal is measured. “We don’t see job losses, but we do see examples where companies have to hire less resources,” she says. AI is quietly shrinking the size of future teams rather than eliminating existing ones, and that distinction matters for an industry employing 338,000 AVFX professionals alone.

The $13.8 billion figure is striking. But what is more striking is the trajectory. The report draws a direct parallel to every major platform era that built $100 billion companies. Search had Google. Social had Meta. Video had TikTok. The interactive era is still up for grabs, and India for the first time has the infrastructure, the user base and the creative momentum to define it.

Also read: One-third of world’s Helium supply gone: How it affects chips to AI chatbots

{kind=link}

{kind=link}

{kind=link}